No, I'm not talking about a Biden or any Democrat.

Scumbags are found the world over. Here is a professional scumbag.

The other day, a friend and I were making our way up the crowded steps of the Acropolis in Athens, Greece. I was leading the way. He felt a tug in his back pocket and quickly turned around to see a guy holding his wallet.

My friend is trained in judo and could have knocked him to his death in an instant. The thief knew he was in danger due to his precarious position on the steps up to the Parthenon. He gave the wallet immediately back to my friend and continued up the stairs. The stairs are all rock, dangerous, slippery, and not OSHA-approved. The stairs are full of people, all moving upward, jostling and often coming in contact with one another. I had moved up to the top and my pal walked up to tell me what had happened. I pulled my phone out and started to photograph this dunce for all the world to see.

If you happen to go to Greece any time soon, watch for this bona fide scumbag.

He was with two others, a guy and gal. They were working in unison.

Here he is trying to get into this guys back pocket. The man in the hat doesn't realize he is being targeted for theft while standing there. This next picture is of him flipping us the bird as he was trying to get the hell out of there. He knew I was taking video of him.

Trump is playing with Wall Street.

Trump is a real estate guy.

Imagine the tentacles of Goldman Sachs working around the clock, in trading, government policy, Congress itself, the legions of lobbyists bought and paid for, all trying to game the system and own the companies that the Donald will pick as being winners.

The United States is now over $38,000,000,000,000.00 in debt.

The interest on that amount is over $1 trillion per year.

So, sit back and enjoy the show. It might come faster than you think.

Compounding interest doesn't lie.

A million seconds ago was October 11thFrom Athens to the high seas, here we come.

I am ready for some rest and recreation for the year. Being in an active trading mode has been a beautiful thing and coming off the deep dive we had last spring has been wondrous. At 71, I wish I had it to do all over again; not much I would change, except the learning curve timeline, and I probably speak for all professionals in that regard.

Never argue with the market. Covered index shorts and reloaded.

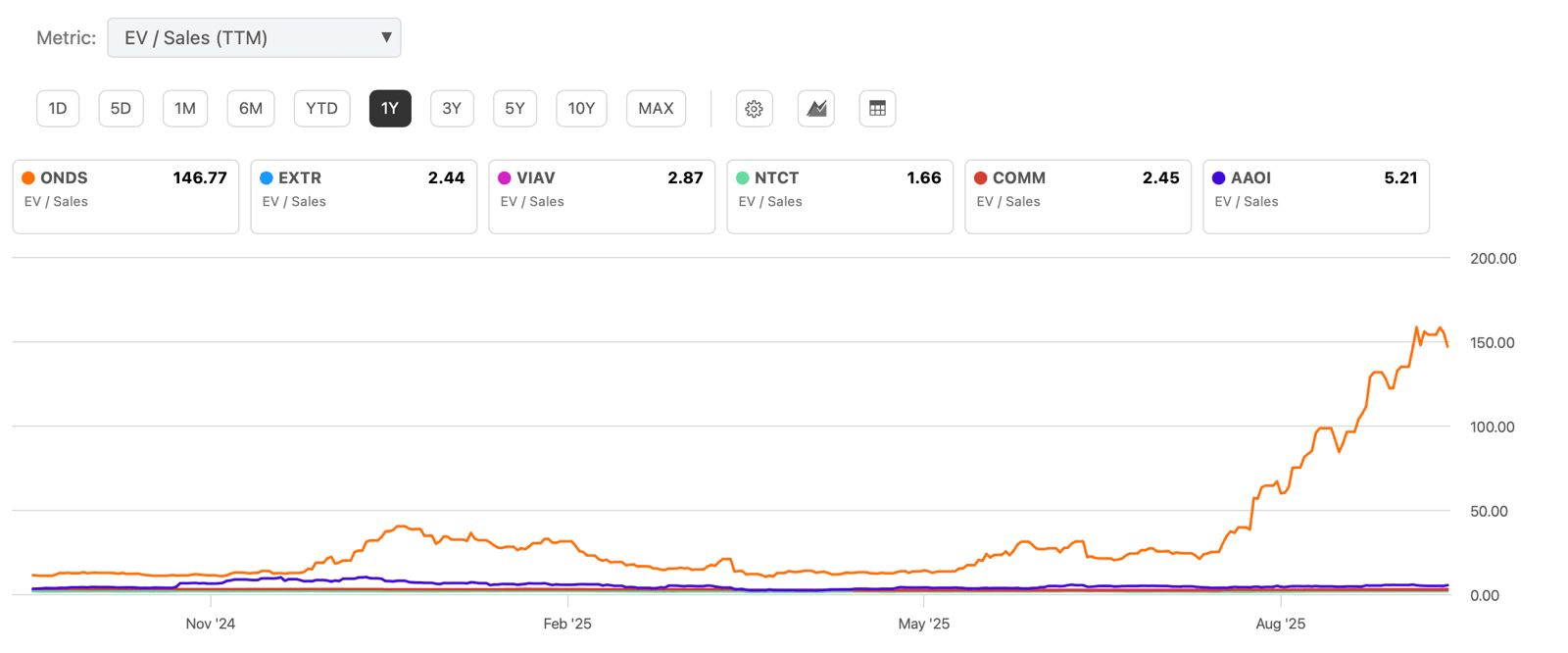

ONDS

Like Bill always said, the big money is made by sitting.

Pyramid.

It's what makes the big money.

This is reprinted without permission from Seeking Alpha.

metamorworks/iStock via Getty Images

Ondas Holdings Inc. (NASDAQ:ONDS) brings about a high-risk, high-reward investment opportunity as the company is situated at the connection between autonomous robotics and industrial wireless infrastructure. Even though the company is still considered small cap, it is still poised for a plausible inflection year in 2025, supported by the latest $230 million capital fundraise, the recently attained defense contracts, as well as deepening cross-border alliances.

Capitalizing on regulatory impetus (including the vital Federal Aviation Administration (FAA) waivers), prominent smart city contracts in United Arab Emirates (UAE) and Tel Aviv, and a strategic rail digitization collaboration with Siemens Mobility, Ondas is actively constructing the foundation of the next-generation autonomous infrastructure. Even if only small-scale projects manage to scale, the business may quickly transition from a cash-burning model to a recurring-revenue platform with heightening gross margins.

Ondas is designedly structured into two key operational segments, which are brought together to form a vertically integrated autonomy infrastructure provider. As a result, the company is in the position to provide both the pivotal communication pillar in addition to the robust robotic systems to permit fully automated operations across mission-critical industries.

To begin with, the Ondas Autonomous Systems (OAS) business division was formed via the acquisitions of Airobotics Ltd. (Israel) and American Robotics, Inc. (United States). This merged entity creates and stations fully self-directed drone and ground robotic solutions designed for defense, smart cities, and industrial customers. All in all, the unit’s main value proposition would be its “drone-in-a-box” system, which allows entirely robot-driven, unmanned operations involving charging, launch, flight as well as landing.

In the meantime, OAS is equipped with numerous competitive advantages that are essential. Firstly, American Robotics has an extremely limited FAA waiver permitting Beyond Visual Line of Sight (BVLOS) operations in the United States (US). On top of that, Airobotics possesses active municipal contracts in high-growth markets such as the UAE and Tel Aviv, which comprises a partnership for the National Defense Authorization Act (NDAA)-compliant combat drones in the US with Rift Dynamics alongside an initial $3.2 million defense contract for ground robotics payloads. Not to mention, the company now also has a newly established facility in Israel that caters for the scalable production of hardware to fuel the expanding defense industry vertical.

On the other hand, the Ondas Networks unit offers Software-Defined Radio (SDR) solutions through its flagship FullMAX platform. In essence, FullMAX facilitates private, crucial wireless networks. This, in turn, permits industrial clients — in particular, those from the energy, utilities, and railroad sectors — to deploy long-term evolution (LTE)-class communications over licensed spectrum in which public networks may be compromised or undependable.

An important stimulus for this division would be its association with strategic partner Siemens Mobility, whereby strategic partner, Siemens Mobility, is integrating its FullMAX SDR system into Ondas Networks’ US rail control system product to streamline Class I railroad communications. Upon the triumphant execution of pilot projects, these integrations are anticipated to shift into the wider commercial deployments commencing late 2025.

Ultimately, the bullish thesis for Ondas depends entirely on the company’s capability in realizing and scaling three central opportunities. These drivers would subsequently imply that the business is finally progressing from a prototype in its research and development (R&D) stage into a multi-vertical commercial platform — resulting in 2025 becoming Ondas’ vital inflection point.

Quintessentially, Ondas’ collaboration with Siemens Mobility is targeting the enormous, multi-billion dollar modernization of the Class I railroad communications infrastructure in the US. The FullMAX SDR system by Siemens Mobility is pivotal in the provision of a steady, exclusive wireless network that is necessary for mission-critical signaling and control applications.

Meanwhile, early-stage deployments — such as the upgrading of Chicago's metropolitan commuter rail, Metra — are focusing on the replacement of the legacy Positive Train Control (PTC) systems. These initiatives are also expedited by federal safety mandates in combination with the strong advocacy for digitised control networks.

Now, with Siemens Mobility aggressively marketing its FullMAX SDR system towards its US-based railway stakeholders, early commercial deployment are forecasted to kickstart towards the end of 2025, thus moving Ondas Networks from its pilot phase to a promising division of continuous infrastructure revenue.

Interestingly, Ondas is the first-mover within the city-scale autonomous drone infrastructure sector. In fact, the company has been actively stationing drone stations for urban surveillance and public safety purposes upon signing a five-year agreement with Tel Aviv back in 2024. This project, in conjunction with present-day operations in the UAE, has started to bring about revenue-generating contracts in Q2 2025.

Given that the company’s drone-in-a-box systems are offered in the form of long-standing Infrastructure-as-a-Service agreements, the business division’s growth rate would be generating a vital recurring top-line base as more cities begin to adopt aerial reconnaissance solutions. Consequently, this vertical is a primary driver behind Ondas’ reiterated 2025 revenue target of $25 million.

Ondas has achieved substantial diversification of its operations into the ground robotics as well as defense sectors in 2025:

Ground Robotics: Ensuing the acquisition of Apeiro Motion Ltd in August 2025, the company has effectively brought in a $3.5 million defense deal for Apeiro-branded Unmanned Ground Vehicles (UGVs) and mission payloads. This thereby officiates Ondas’ entry into the rugged ground robotics market.

Combat Drones: Ondas’ strategic investment into the Norwegian defense technology firm, Rift Dynamics, resulted in the business securing exclusive US distribution rights for the NDAA-compliant WÅsp combat drone platform. With that, the earliest batch of 500 units are already in place for initial delivery starting in October 2025.

Large-Scale Manufacturing: These novel defense verticals are underpinned by Ondas’ manufacturing facility in Israel, which went into full operation in late 2024. Essentially, this facility is paramount for the company to build a production line that is scalable and margin-friendly across all ground-based and aerial robotics.

Excitingly, Ondas has declared its strongest quarterly performance to date in Q2 2025. In particular, the business has roped in a total revenue of $6.27 million, representing a magnificent year-over-year (YoY) increment of 555%.

Most importantly, the Q2 period also recorded an impactful step-change in the business's profitability standpoint. Specifically, gross profit hit the $3.33 million mark and translated to a gross margin of 52.7%, which is a huge improvement in contrast to the gross loss reported in Q2 2024. This accelerated margin widening can be greatly attributed to a more favorable revenue mix that is fueled mainly by the long-term federal and municipal Infrastructure-as-a-Service drone deployment contracts.

As investors glance into the future, the management has restated its full-year FY2025 top-line guidance of $25 million, citing enhanced visibility and solid execution capabilities as primary drivers. This conviction is ultimately reinforced by the record-setting backlog of $22 million, which props up the revenue conversion into Q3 and Q4 2025.

Even though the documented operating costs of $12.6 million has led to an operating loss of $9.2 million, this activity is consistent with a business that is prioritising aggressive upscaling. That said, the leadership has effectively derisked the company’s image via the successful $230 million equity raise back in September 2025. Overall, this cash infusion supplies the firm with an extended 12- to 18-month operational runway so that the management can concentrate intently on their backlog conversion, execution, and production scaling without having to worry about finances in the near-term.

In short, the valuation for Ondas may be considered to be extremely stretched.

Based on the data as at September 2025, the company’s stock has been substantially outpacing its industry peers, trading at a trailing twelve month (TTM) Enterprise Value to Sales (EV/Sales) multiple of 146.77×:

Seeking Alpha

While Ondas’ unique standing in the autonomous infrastructure segment alongside its thrilling growth prospects validates a premium, this extensive gap between the firm and its peers signifies considerable optimism and leaves virtually negligible room for any mistakes.

Should we apply a still-generous TTM EV/Sales multiple of 20× to Ondas’ $16.1 million TTM revenue, the proposed enterprise value (EV) would thereby be around $322 million. With reference to the present stock count of 101.5 million, this would lead us to $3.17 as the fair share price. And based on the current share price of $7.41, this presents a 57% downside risk as a possibility.

In other words, this means that the market has already priced in the business’s extraordinary growth across all industry verticals simultaneously. Hence, any slowdowns in project execution and/or behind schedule revenue ramp-ups is most likely going to spark a significant re-rating.

As a result, in spite of my hope in the company’s long-term growth story, Ondas’ present-day valuation is far too stretched to warrant a bullish stance. Thus, I have decided to assign a Hold rating for the time being.

Besides that, although Ondas presents plenty of room for growth, investors need to understand that the business still faces numerous regulatory, operational, and financial challenges. Considering that the company’s heightened valuation leaves zero margin for error, this thereby justifies the careful monitoring of acute risks that may derail the growth story.

Although the company has a sturdy client pipeline, it remains important to acknowledge that Ondas is still pivoting from the running of pilot programmes to full-scale, recurring contracts. Hence, any hindrance in translating the backlogs from Siemens Mobility, Tel Aviv, or the US defense sector may expose the share price to sharp corrections due to the firm’s ongoing cash burn and elevated fixed costs.

In essence, investors are basically making weighty bets on Ondas’ flawless, simultaneous top-line increments across all of its sector verticals.

Ondas business operations, including constructing drone stations, stationing radio networks, and developing robotics, is highly capital-intensive. Even though the newly raised $230 million keeps the firm buoyant for the time-being, Ondas is still vulnerable to the likelihood of having to raise additional capital if its revenue growth rate remains insufficient to offset the operational expenses.

Moreover, the future equity raises bear the risk of significantly eroding shareholder returns as there are already 101.5 million shares outstanding (which already marks a notable YoY rise from 69.9 million shares outstanding).

A noteworthy portion of the company’s growth prospects remain sensitive to government procedures. This comprises matters such as the critical FAA waivers for BVLOS operations, municipal contracts, as well as the procurement cycles for the defense sector.

Consequently, any amendments to the FAA policy, realignments to the defense budget, or volatility in the political environment of key markets may adversely impact the deployment rate, leading to potential delays or even cancellations. So, this heavy dependence on a focused group of public sector customers makes the company’s top line relatively less foreseeable as opposed to private technology players.

All in all, Ondas is in an excellent position to capitalise the high growth potential of its niches — whether it is regarding artificial intelligence or autonomous robotics — as part of securing wireless networks for critical infrastructure. Furthermore, the municipal deployments, defense sector contract victories, and strong ties with Siemens Mobility all imply a business foundation that have been meticulously crafted for a major revenue inflection.

Still, it is evident that investor expectations have run ahead of fundamentals. Taking into account that Ondas’ shares have been trading at approximately 150× revenue multiple and that the journey to achieving consistent profitability is heavily contingent on future executions, the stock could be deemed aggressively priced.